Credit cards can be a powerful financial tool, but it’s crucial to understand how to manage them effectively. The question of “How many credit cards are too many?” is not as simple as it might seem and varies from person to person.

Therefore, let’s explore this topic further and ask some critical questions.

Key Takeaways

- There isn’t a set number of credit cards that is universally deemed “too many.”

- The average American has around five credit cards.

- It’s not necessarily the number of cards you have, but how you use them that matters most.

Credit Card Statistics in the U.S.

| Description | Average Number |

|---|---|

| Average number of credit cards per person | 5 |

| The number of credit cards is considered ‘too many’ for most people | 7 |

What should be the Ideal Number of Credit Cards?

The ideal number of credit cards varies greatly from person to person. It depends on individual credit needs, financial habits, and the ability to manage multiple accounts responsibly.

Evaluating Your Credit Card Readiness

Before you apply for another credit card, it’s important to evaluate your readiness.

Consider your past financial habits:

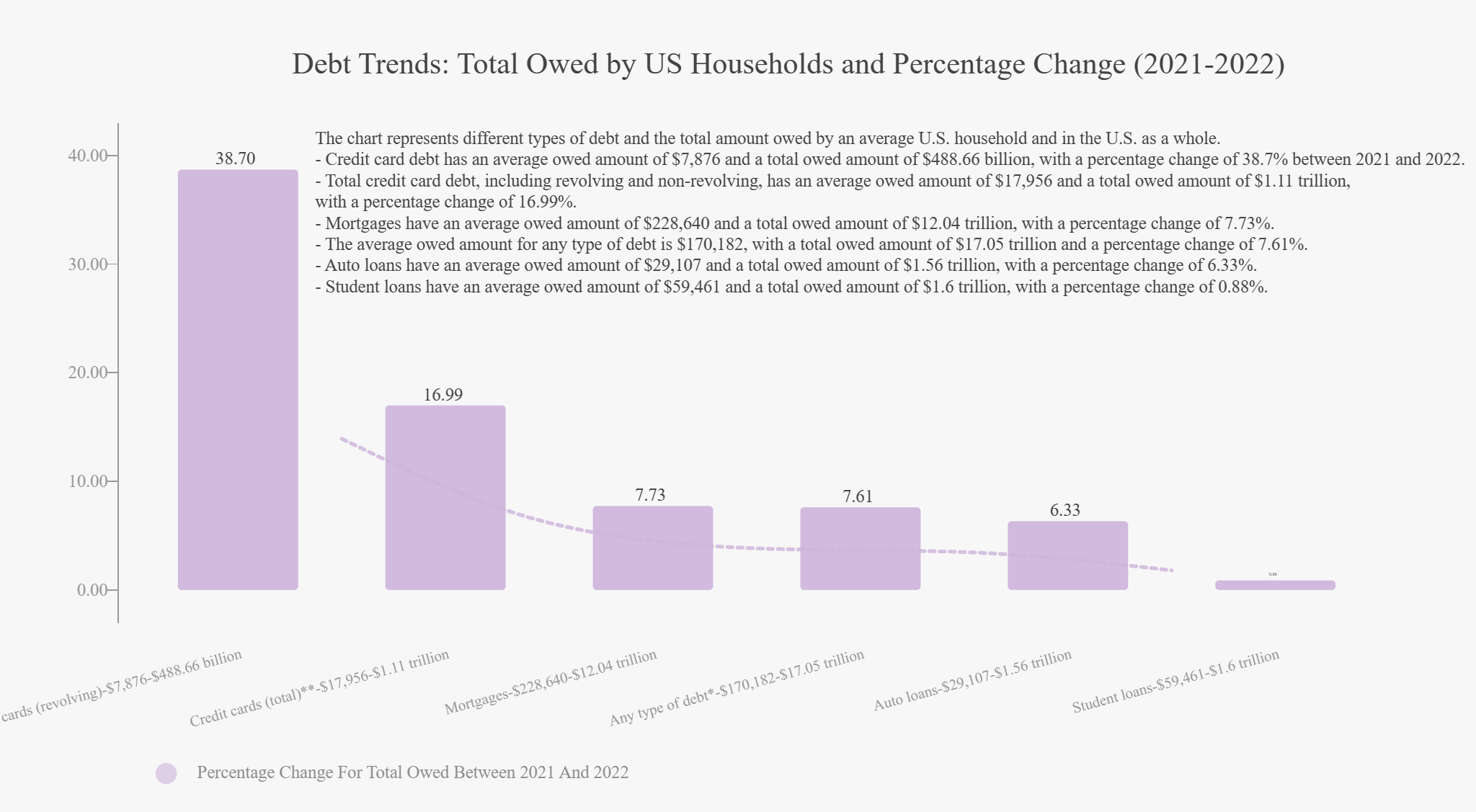

Do you have a history of overspending or struggling with debt? If so, adding another credit card might exacerbate the issue unless you’ve taken steps to address these behaviors. In fact, as of 2022, the average credit card debt per U.S. household was $5,525.

Do you have recently applied for Credit Cards?

Another crucial aspect to understand is the impact of new credit applications on your credit score. Each time you apply for a new credit card, a hard inquiry is made on your credit report, which can temporarily lower your credit score.

According to FICO, one additional hard credit inquiry typically lowers a person’s credit score by fewer than five points. However multiple inquiries within a short period can compound this effect, signaling to lenders that you may be a higher-risk borrower.

It’s also worth noting that handling multiple credit cards is common. A survey from Experian found that, on average, Americans have four credit cards. However, whether this is beneficial or detrimental depends on individual financial habits and circumstances.

Factors to Consider to Determine, How may Credit card is too much.

Here are some factors to consider when determining how many credit cards may be too many for you:

-

Your Ability to Manage Multiple Cards: Can you effectively track the various due dates, interest rates, and reward systems of multiple cards? If not, having too many could lead to missed payments or overspending.

-

Your Credit Utilization Ratio: This is the amount of credit you’re using compared to your total available credit. A lower ratio is better for your credit score. Having more credit cards could potentially improve this ratio, as long as you don’t increase your spending proportionally.

-

Your Credit History: Each time you apply for a new credit card, a hard inquiry is made on your credit report, which can temporarily lower your credit score. However, a longer credit history with well-managed accounts can contribute positively to your score.

-

Your Financial Needs and Habits: The number of cards you should have also depends on your lifestyle and spending habits. If you frequently travel or spend in specific categories, like dining or groceries, having multiple credit cards offering rewards in these areas could be beneficial.

Conclusion

The number of credit cards that are considered “too many” largely depends on your financial situation and your ability to manage credit responsibly.

It’s less about the quantity and more about the quality of your credit management practices.

So, how can you improve your credit utilization ratio? Reflect on this question as you consider your credit card strategy.